Introduction

Closing a company in the UAE involves more than cancelling a trade licence. A successful company liquidation in UAE requires legal, tax, and accounting obligations to be completed in parallel, and failing to complete any one of these requirements can delay the final licence cancellation certificate.

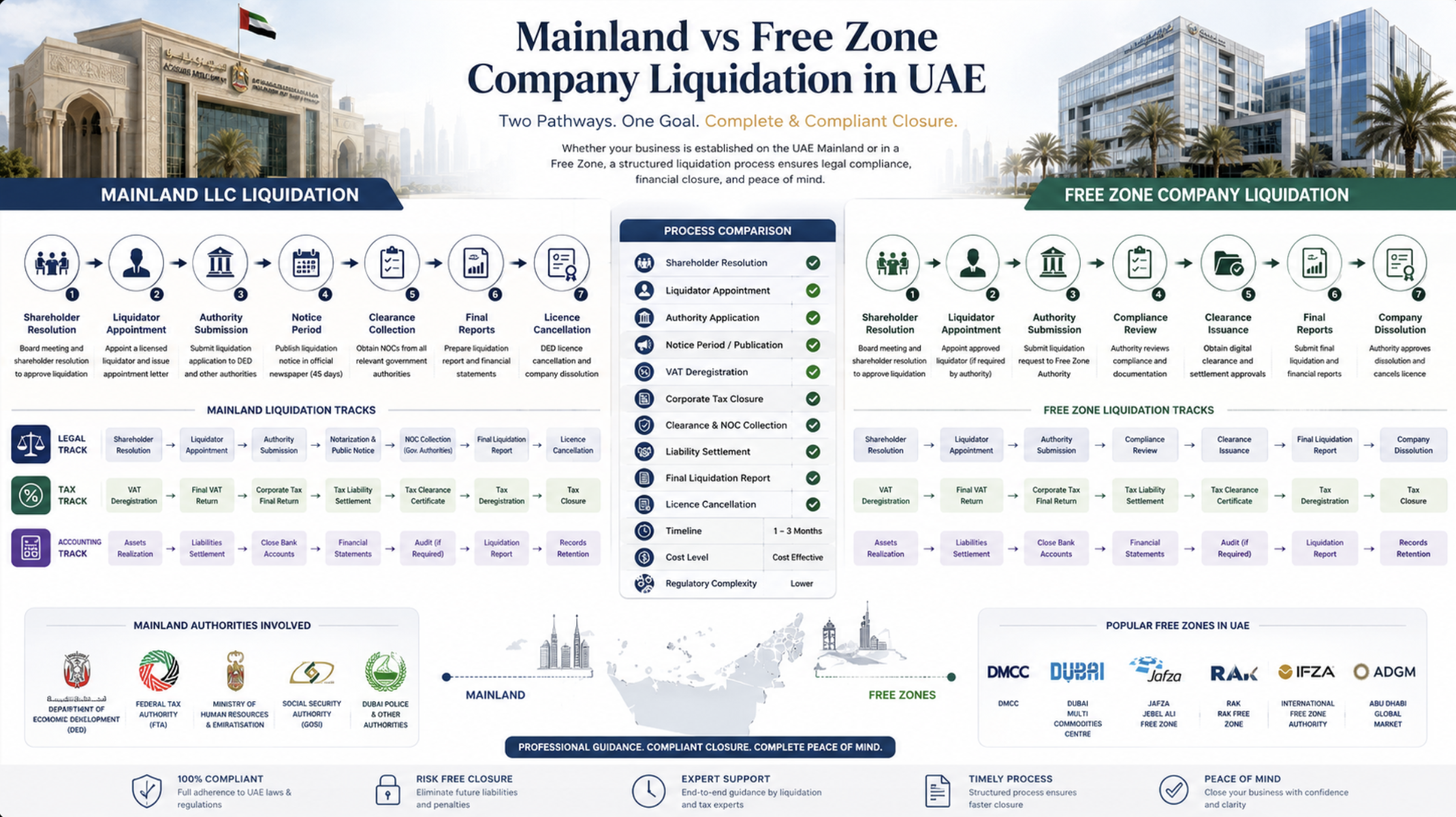

Whether you are liquidating a company on the mainland or in a free zone, the process typically involves shareholder approvals, liquidator appointments, regulatory clearances, VAT deregistration, corporate tax compliance, final accounts preparation, and licence cancellation procedures. Multiple authorities may be involved, including the licensing authority, the Federal Tax Authority (FTA), banks, utility providers, and immigration authorities.

This guide explains the full UAE company liquidation process for both mainland LLCs and free zone entities. It covers the legal liquidation steps, VAT deregistration requirements, corporate tax obligations, final accounts preparation, audit and clearance requirements, and the documents typically required before a company can be formally closed.

What Is Company Liquidation in the UAE?

The liquidation of a company in the UAE is the formal process of winding up business operations, settling liabilities, distributing any remaining assets, and cancelling the trade licence. Once the liquidation process is completed, the company ceases to exist as a legal entity.

A company may enter liquidation because shareholders decide to close the business, operations are no longer commercially viable, the company has fulfilled its purpose, or a court orders its closure. Regardless of the reason, the process must comply with the requirements of the relevant licensing authority and applicable UAE laws.

Before starting the company liquidation process in UAE, business owners should understand the following distinctions:

- Voluntary liquidation occurs when shareholders decide to close the company and appoint a liquidator to manage the winding-up process.

- Compulsory liquidation occurs through a court order, typically arising from insolvency proceedings, creditor claims, or other legal disputes.

- Deregistration is generally a simpler administrative licence-cancellation process available in limited circumstances where full liquidation may not be required.

- Full liquidation is a more comprehensive process that typically involves a shareholder-appointed or court-appointed liquidator, settlement of liabilities, preparation of final accounts, and collection of clearance certificates before licence cancellation.

The liquidation process can apply to mainland LLCs, free zone companies, offshore entities, and certain branch offices, subject to the requirements of the relevant authority.

While procedures vary between jurisdictions, the objective remains the same: settle obligations, close registrations, obtain regulatory clearances, and secure final licence cancellation. Understanding what is the process of liquidating a company provides the foundation for navigating the legal, tax, and accounting requirements that follow.

Overview of the UAE Company Liquidation Process

While documentation requirements vary by authority, the overall company liquidation process in UAE follows a similar sequence for both mainland and free zone entities. The key point many business owners overlook is that legal, tax, and accounting obligations must be managed in parallel. Waiting until the end of the process to address VAT deregistration, Corporate Tax compliance, or final accounts can delay licence cancellation and regulatory clearances.

The typical UAE company liquidation process includes:

Shareholder Resolution

Shareholders formally approve the decision to liquidate the company and appoint a liquidator where required.

Liquidator Appointment

The liquidator assumes responsibility for overseeing the winding-up process, settling liabilities, preparing reports, and coordinating the liquidation procedure.

Authority Submission

Initial liquidation documents are submitted to the relevant authority, such as the Department of Economy and Tourism (DET) for mainland entities or the applicable free zone authority.

Newspaper Notice Period

Where required, a public notice is published to allow creditors to submit claims within the prescribed notice period.

Parallel Clearance Procedures

The company begins obtaining clearances from government authorities, banks, utility providers, landlords, and other relevant parties. VAT and Corporate Tax obligations should also be addressed during this stage rather than after the legal process concludes.

Final Accounts and Audit

Final financial statements, liquidation accounts, and supporting reports are prepared. Where required, these documents are reviewed and certified by the appointed liquidator.

Final Licence Cancellation

Once all liabilities are settled, clearances obtained, and regulatory requirements completed, the authority issues the final licence cancellation certificate and the company is formally dissolved.

This framework applies broadly to mainland LLCs and free zone companies, although notice periods, approval requirements, documentation, and fees vary by authority. Businesses should confirm specific requirements with the relevant licensing authority before starting the liquidation process.

Mainland LLC Liquidation: Step-by-Step

The mainland company liquidation in UAE process generally follows two phases. While specific requirements may vary by emirate, the overall framework remains similar.

Phase 1: Resolution, Liquidator Appointment, and Initial Dissolution

The liquidation of LLC company in UAE begins with a shareholder resolution approving the closure of the company and appointing a liquidator. For mainland entities, this is typically documented through notarised General Assembly minutes.

The initial submission commonly includes:

- Notarised General Assembly minutes confirming liquidation

- Shareholder resolution approving liquidation

- Liquidator acceptance letter

- Supporting company documents required by the Department of Economy and Tourism (DET) or relevant authority

Following approval and payment of the applicable fees, the authority issues an initial dissolution certificate.

A public notice is then generally published in two Arabic daily newspapers, with one publication in each newspaper. A 45-day creditor claim period follows, allowing creditors to submit claims before the company proceeds to final cancellation.

Phase 2: Final Liquidation and Licence Cancellation

Once the creditor notice period has expired and outstanding matters have been addressed, the company can proceed with the final stage of liquidation.

Typical requirements include:

- Final liquidation report prepared by the liquidator

- Liquidator declaration of no objection

- Partners’ or shareholders’ declaration of no objection

- Labour card cancellation through the Ministry of Human Resources and Emiratisation (MOHRE)

- Visa cancellation confirmations and other required clearances

- Submission of final documents for licence cancellation

After all requirements have been satisfied, the authority issues the final licence cancellation certificate.

Under Federal Law No. 2 of 2015, the company’s auditor cannot be appointed as the liquidator at the time of appointment or if they served as the company’s auditor within the previous five years. This restriction is intended to preserve the independence of the liquidation process.

Free Zone Company Liquidation

A free zone company liquidation in UAE follows the same core objective as mainland liquidation: settle liabilities, complete regulatory clearances, prepare final accounts, and obtain approval from the relevant authority before deregistration.

However, each free zone authority maintains its own forms, procedures, timelines, and fee schedules. Requirements vary between authorities such as JAFZA, DMCC, RAKEZ, IFZA, DIFC, and ADGM, so businesses should confirm the applicable process with their licensing authority.

For most standard free zones, the company liquidation process in UAE generally follows this sequence:

- Shareholders approve a liquidation resolution.

- A liquidator is appointed where required.

- Initial liquidation or deregistration documents are submitted.

- Employee, immigration, banking, lease, utility, and tax clearances are completed.

- Final accounts and the liquidator’s report are prepared.

- The authority issues the final deregistration or licence cancellation certificate.

Unlike mainland LLC liquidation, most free zones do not require Notary Public notarisation of the shareholders’ resolution. Instead, resolutions are typically executed under the free zone’s own corporate governance requirements.

Companies should also note that requirements may differ regarding liquidator qualifications, employee and visa clearances, lease termination procedures, audit requirements, and supporting documentation.

Additional considerations apply to DIFC and ADGM. These jurisdictions operate under separate common-law frameworks with their own winding-up regulations, and professional insolvency practitioners are often required.

Regardless of the authority, VAT deregistration, Corporate Tax obligations, final accounts, and regulatory clearances should be completed alongside the legal liquidation process to avoid delays in obtaining final deregistration approval.

VAT Deregistration When Closing a UAE Company

VAT deregistration is a key compliance requirement during company liquidation in UAE. Closing a trade licence does not automatically cancel a company’s VAT registration. Businesses that cease making taxable supplies must separately apply for VAT deregistration with the Federal Tax Authority (FTA).

Under UAE VAT regulations, a taxable person must apply for VAT deregistration within 20 business days of ceasing to make taxable supplies.

The process is completed through the EmaraTax portal and generally includes the following steps:

- Submit a VAT deregistration application.

- Confirm the effective date on which taxable supplies ceased.

- File the final VAT return covering the period up to that date.

- Settle any outstanding VAT liabilities or administrative penalties.

- Respond to any FTA requests for additional information or supporting documentation.

Before submitting the application, businesses should ensure that all VAT returns have been filed and that VAT balances reconcile with the underlying accounting records. Unfiled VAT returns, unpaid VAT liabilities, or outstanding penalties can prevent deregistration from being approved and must be resolved first.

Once the FTA is satisfied that all VAT obligations have been met, it issues a VAT deregistration confirmation. This confirmation is typically required as part of the liquidation file before the licensing authority will issue the final licence cancellation certificate.

For additional guidance, see our guide to VAT deregistration in the UAE.

Because VAT clearance forms part of the broader tax on liquidation of company obligations, businesses should review their VAT position early in the liquidation process rather than waiting until the final stages of closure.

Corporate Tax Obligations on Company Closure

Corporate Tax obligations continue during the liquidation process. Closing a company does not automatically end its tax responsibilities, and businesses must complete both filing and deregistration requirements with the Federal Tax Authority (FTA).

Under the UAE Corporate Tax Law, a liquidating company must file a final Corporate Tax return covering the tax period up to the effective liquidation date. The return should reflect taxable income earned during that period based on the company’s final accounting records.

When assessing corporate tax on company closure UAE, businesses should also consider transactions that occur during the winding-up process. Depending on the circumstances, gains arising from asset disposals or distributions made during liquidation may form part of taxable income.

Key Corporate Tax obligations include:

- Preparing final accounting records and tax calculations.

- Completing UAE corporate tax return filing requirements for the liquidation period.

- Reviewing gains arising from asset disposals and distributions during winding up.

- Settling any outstanding Corporate Tax liabilities.

After the final return has been filed and accepted, the company must submit a Corporate Tax deregistration request to the FTA. Deregistration is only granted once all filing obligations, tax liabilities, and compliance requirements have been satisfied.

Because tax on liquidation of company obligations continue until deregistration is completed, businesses should address Corporate Tax requirements alongside the legal and accounting aspects of liquidation rather than leaving them until the final stages of closure.

Final Accounts, Audit, and Clearance Certificates

Final accounts and clearance certificates are a critical stage in the company liquidation process in UAE. Before a licensing authority issues the final licence cancellation certificate, the company must demonstrate that its liabilities have been settled, financial records have been finalised, and all required clearances have been obtained.

The final liquidation report is typically supported by final audited financial statements, including:

- A balance sheet as at the cessation or liquidation date.

- A statement of affairs showing assets realised, liabilities discharged, and any distributable surplus.

- Supporting reconciliations and schedules for material balances.

Depending on the entity type and jurisdiction, businesses may also need to comply with applicable audit requirements for UAE companies.

The liquidator reviews the company’s financial records, certifies the final accounts, and signs the liquidation report submitted to the licensing authority. In practice, the liquidator is typically a registered auditor or licensed insolvency practitioner authorised to perform the engagement under the applicable regulatory framework.

Before final approval can be granted, statutory clearances are generally required from:

- Immigration Department (visa cancellations)

- MOHRE (labour card cancellations)

- DEWA or the relevant utility authority

- Telecom providers

- Landlords or property managers

- Banks (account closure confirmation)

- Federal Tax Authority (VAT and Corporate Tax clearance)

Businesses should also ensure that corporate records are properly updated or closed, including any outstanding UBO registration and compliance requirements.

For mainland company liquidation in UAE, collecting these clearances during the creditor notice period rather than at the final submission stage can significantly reduce delays. Running legal, tax, accounting, and clearance activities in parallel generally shortens the overall liquidation timeline.

Common Mistakes That Delay UAE Company Liquidation

ost delays during UAE company liquidation are caused by unresolved compliance requirements rather than the legal liquidation procedure itself.

Common issues include:

- Applying for FTA VAT deregistration before filing all outstanding VAT returns or settling VAT liabilities and penalties. The FTA will generally not complete deregistration until these obligations have been resolved.

- Submitting Phase 2 liquidation documents before employee visas and labour cards have been cancelled through the relevant authorities, including MOHRE and Immigration.

- Filing the final Corporate Tax return but failing to submit the subsequent Corporate Tax deregistration request to the FTA.

- Appointing the company’s existing auditor as the liquidator, or appointing an individual who served as the company’s auditor within the previous five years, which is prohibited for mainland LLC liquidations.

- Following mainland Department of Economy and Tourism (DET) procedures for a free zone entity. Authorities such as JAFZA, DMCC, RAKEZ, IFZA, DIFC, and ADGM maintain their own liquidation requirements, forms, and approval processes.

- Delaying final accounts, clearance certificates, bank closure letters, and tax clearances until the final submission stage.

When liquidating a company, legal, tax, accounting, and clearance requirements should be managed in parallel. Businesses that address VAT deregistration, Corporate Tax obligations, employee clearances, and financial reporting early typically experience a smoother UAE company liquidation process with fewer delays.

Company liquidation in UAE requires more than licence cancellation. Businesses must coordinate legal, tax, accounting, and regulatory requirements while meeting the expectations of the relevant licensing authority and the Federal Tax Authority (FTA).

MP Elites supports businesses throughout the liquidation process by assisting with:

- Liquidator coordination and liquidation reporting requirements.

- VAT deregistration applications and final VAT return preparation.

- Final Corporate Tax filing obligations and tax deregistration procedures.

- Preparation of final accounts and supporting financial documentation.

- Coordination of clearance requirements, including tax, banking, employment, and regulatory records.

Whether you are closing a mainland LLC or a free zone entity, early planning can help reduce delays, resolve compliance issues, and support a smoother closure process.

To discuss your company’s liquidation requirements, contact MP Elites for guidance tailored to your business structure, licensing authority, and compliance obligations.

Frequently Asked Questions

How long does company liquidation in the UAE typically take?

The timeline varies by company type, licensing authority, and the time required to obtain regulatory clearances. For mainland companies, the mandatory 45-day creditor notice period is often a key factor. Delays in VAT deregistration, Corporate Tax compliance, visa cancellations, or bank account closures can extend the process.

Do I need to file a final VAT return before applying for FTA deregistration?

Yes. Businesses must file all outstanding VAT returns and settle any VAT liabilities or penalties before the Federal Tax Authority (FTA) will approve VAT deregistration. Businesses that cease making taxable supplies must generally apply for deregistration within 20 business days.

What happens to Corporate Tax obligations when a UAE company is liquidated?

A liquidating company must file a final Corporate Tax return covering the tax period up to the effective liquidation date. Once all filing obligations and tax liabilities have been settled, the company can submit a Corporate Tax deregistration request to the FTA.

Can the company’s existing auditor act as the liquidator in a UAE LLC?

No. For mainland LLC liquidations, the company’s current auditor cannot be appointed as the liquidator. This restriction generally also applies to auditors who served the company within the previous five years.

What clearance certificates are required before the final licence cancellation certificate is issued?

Requirements vary by authority, but commonly include clearances from Immigration, MOHRE, utility providers, telecom providers, landlords, banks, and the FTA. These confirm that employment, contractual, financial, and tax obligations have been properly closed.

Is the liquidation process different for mainland and free zone companies in the UAE?

The overall process is similar, including shareholder approval, liquidator appointment, tax compliance, final accounts, and deregistration. However, each free zone authority, including JAFZA, DMCC, RAKEZ, IFZA, DIFC, and ADGM, maintains its own procedures, forms, and documentation requirements.