VAT deregistration in the UAE is the process of cancelling a business's VAT registration with the Federal Tax Authority when it is no longer required to remain registered. This applies when a business stops making taxable supplies, its taxable turnover falls below the applicable threshold, or the business is closed or liquidated.

Understanding VAT deregistration in UAE is important because it does not happen automatically. A business remains registered until it submits a deregistration application and receives approval from the Federal Tax Authority. Even if operations have stopped, VAT obligations continue until deregistration is completed.

Businesses are required to apply for deregistration within the prescribed timeframe. Failure to apply on time may result in administrative penalties, based on current FTA schedules. Acting within the required timeframe helps reduce compliance risk and ensures obligations are properly closed.

Mandatory vs. Voluntary VAT Deregistration

The first step in the deregistration of VAT in UAE is determining whether the situation falls under mandatory or voluntary deregistration.

Mandatory deregistration applies when:

- The business has stopped making taxable supplies

- Taxable turnover has fallen below AED 187,500 over the previous 12 months

In these cases, the business must apply for deregistration with the Federal Tax Authority. This is a requirement, not an option. The application must be submitted within the prescribed timeframe set by the authority.

Voluntary deregistration applies when:

- Taxable turnover is below AED 375,000 but above AED 187,500

In this range, deregistration is optional. Businesses may choose to remain registered or apply for UAE VAT deregistration based on their operational needs.

The key difference is the level of obligation. Where mandatory conditions are met, the business is required to act within the required timeframe. Understanding these thresholds is central to meeting VAT deregistration requirements in UAE and avoiding compliance issues.

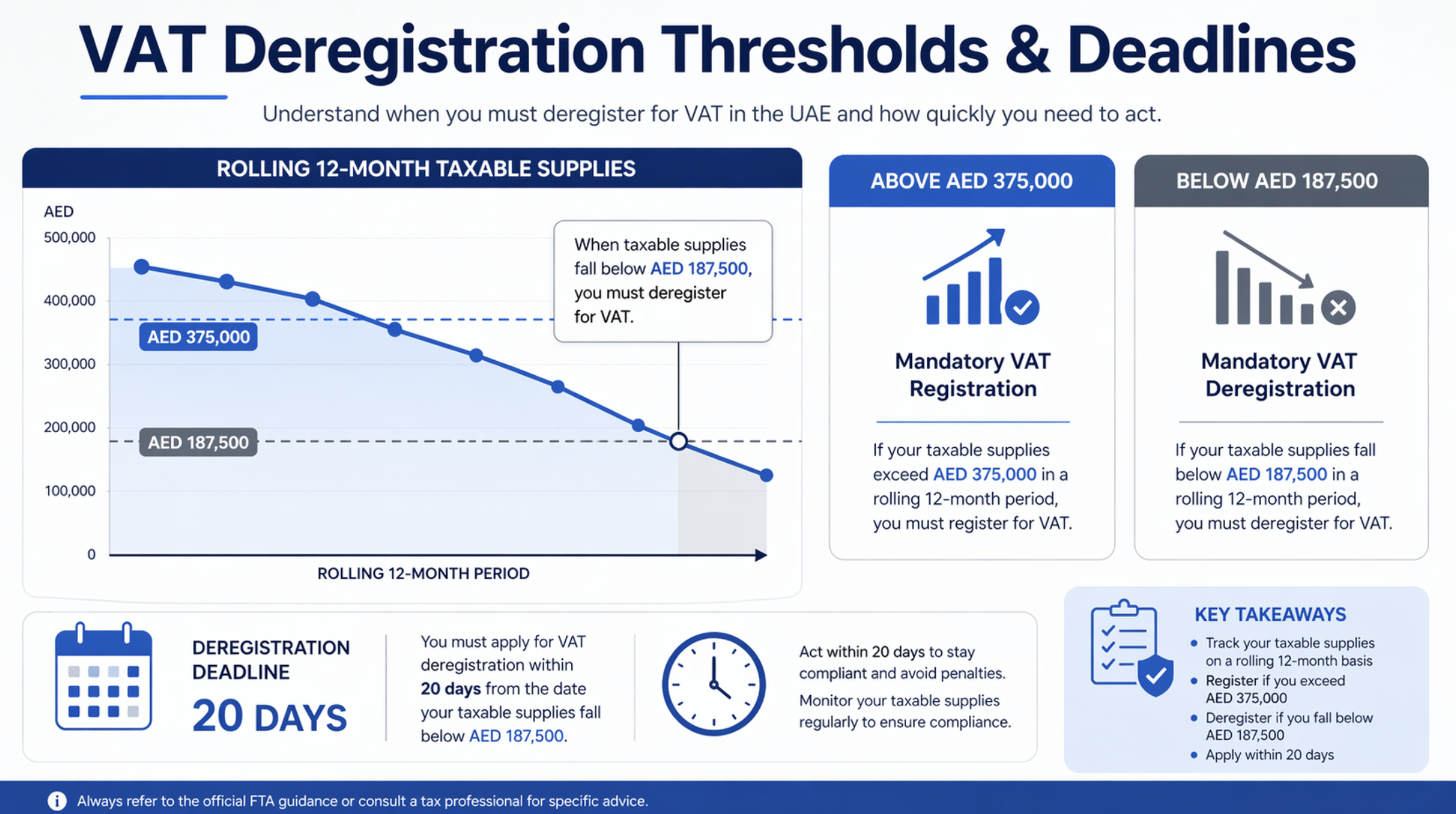

VAT Deregistration Thresholds and Timing Rules

Once eligibility is identified, the next step is timing. The VAT deregistration process in UAE is governed by defined thresholds and deadlines set by the Federal Tax Authority.

Thresholds

- Mandatory deregistration threshold: Taxable turnover below AED 187,500

- Voluntary deregistration range: Between AED 187,500 and AED 375,000

Timing rules

- Deadline to apply: Within 20 business days from the date the business becomes eligible

Eligibility is triggered when:

- The business stops making taxable supplies

- Taxable turnover falls below the relevant threshold based on a rolling 12-month period

This rolling calculation is important. It is based on the most recent 12 months of activity, not a fixed calendar year.

Failure to apply within the required timeframe may result in administrative penalties, based on current FTA schedules. VAT registration remains active until the deregistration application is submitted and approved.

Penalties for Late or Missing Deregistration

Delays in UAE VAT deregistration can result in an administrative penalty of AED 10,000, based on current guidance from the Federal Tax Authority.

This penalty may apply when a business does not submit a deregistration application within 20 business days of becoming eligible. The timing is based on when eligibility is triggered, not when the business decides to apply.

Common situations where businesses may face penalties include:

- The business has stopped trading but remains VAT registered

- Registration is assumed to cancel automatically after inactivity

- Taxable turnover falls below AED 187,500, but no application is submitted

Even if operations have ceased, VAT obligations continue until deregistration is approved. Understanding how VAT deregistration penalty UAE applies helps reduce the risk of avoidable penalties.

Required Documents for VAT Deregistration

Before starting the application, it is important to prepare the documents required under VAT deregistration requirements in UAE. Requirements may vary depending on the case and should be confirmed through the Federal Tax Authority portal.

Core documents typically required:

- Valid trade license issued by the relevant authority, such as the Dubai Department of Economy and Tourism or the applicable free zone authority

- Financial statements showing taxable turnover

- VAT return history submitted through the EmaraTax system

- Stated reason for deregistration

Additional documents that may be requested:

- Proof of business closure or cessation of activity

- Liquidation or company closure documents, if applicable

- Supporting records showing that taxable supplies have stopped

In some cases, the Federal Tax Authority may request a written explanation to support the application. Preparing a clear supporting statement, similar to a VAT deregistration letter format UAE, can help avoid follow-up queries.

All documents should be accurate and consistent with prior VAT filings submitted through EmaraTax. Incomplete or inconsistent submissions may delay the VAT deregistration process in UAE or lead to additional review requests.

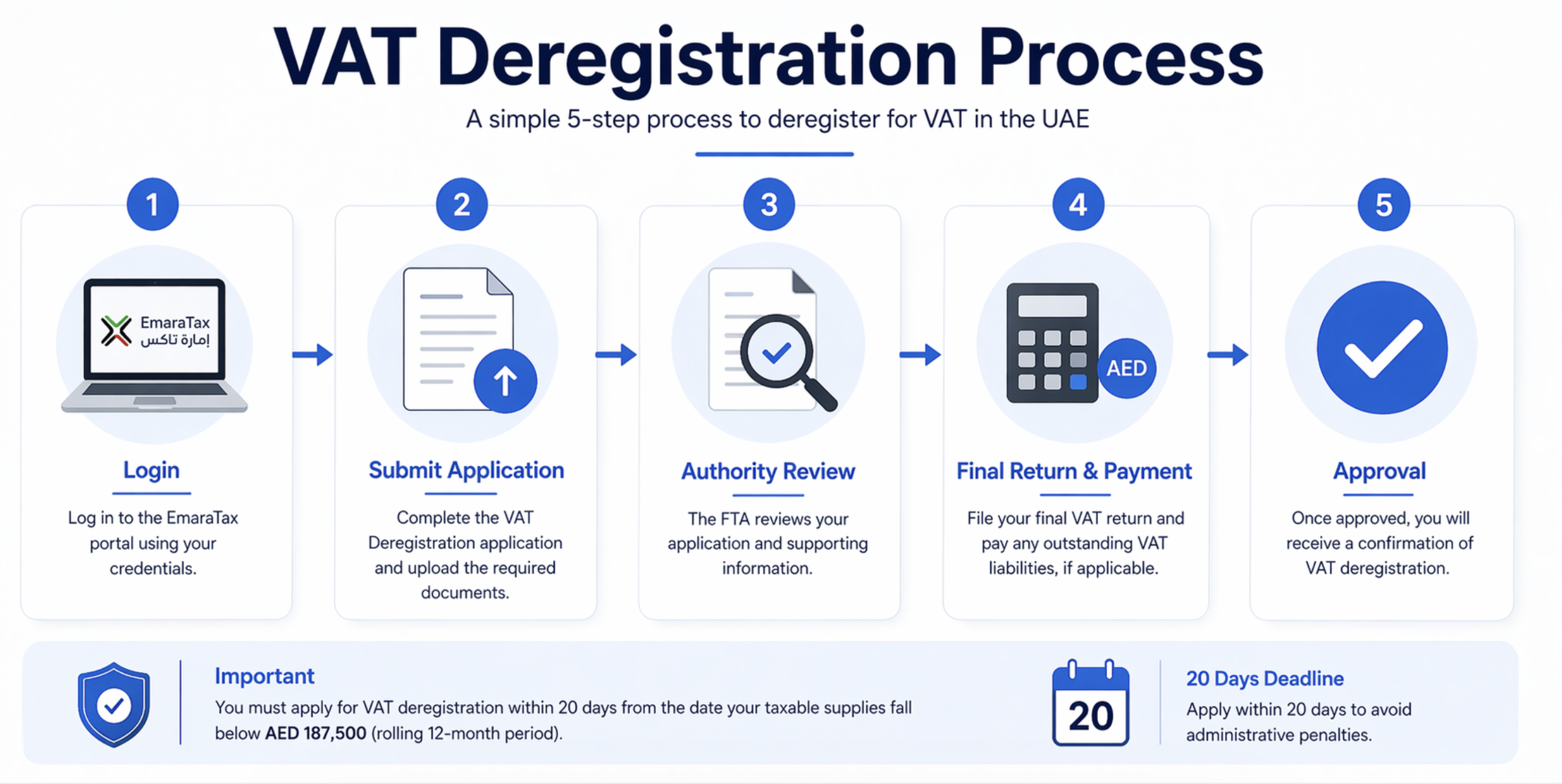

The VAT Deregistration Process Step by Step

Once your documents are ready, you can begin the VAT deregistration process in UAE through the EmaraTax portal managed by the Federal Tax Authority.

Step 1: Log in to EmaraTax

Access your VAT account and select the deregistration option within the system.

Step 2: Submit your application

Enter the required details, including the reason for deregistration and relevant financial information. Upload all supporting documents in line with VAT deregistration requirements in UAE.

Step 3: FTA review

The Federal Tax Authority reviews the application and may request additional information or clarification before proceeding.

After submission

There are additional steps that must be completed before deregistration is finalized:

- Final VAT return: A final return must be submitted covering the period up to the effective deregistration date

- Settlement of liabilities: Any outstanding VAT, penalties, or adjustments must be cleared

- Tax clearance: The Federal Tax Authority confirms that all obligations have been met before approving deregistration

The overall timeline may vary depending on the completeness of the application and the review process. VAT registration remains active until the deregistration is formally approved.

Common Mistakes to Avoid

Even with a clear process, common mistakes can delay approval or lead to penalties during VAT deregistration in UAE.

- Applying before submitting all VAT returns: The Federal Tax Authority will not process a deregistration request if prior VAT filings are incomplete.

- Not filing the final VAT return: A final VAT return must be submitted covering the period up to the deregistration date. Missing this step can delay approval.

- Using the wrong turnover period: Eligibility should be assessed based on a rolling 12-month period, not a fixed financial year. Incorrect calculations can lead to applying at the wrong time.

- Missing or incomplete supporting documents: Inconsistent records or incomplete submissions may result in additional queries from the Federal Tax Authority and delay the process.

Ensuring that filings, calculations, and documentation are complete before applying helps reduce delays and supports a smoother VAT deregistration process in UAE.

FAQs

Can I re-register for VAT after deregistering?

Yes. You must apply for VAT registration again if your taxable turnover exceeds AED 375,000 within a 12-month period, based on current thresholds set by the Federal Tax Authority. Monitoring your turnover regularly helps ensure you meet registration requirements on time.

What happens to input tax credits after deregistration?

You may need to adjust any remaining input tax in your final VAT return. This can apply to assets or inventory you still hold at the time of deregistration. The Federal Tax Authority requires these adjustments before approving your application.

How long does the VAT deregistration process take?

Processing times can vary depending on how complete your application is and the review by the Federal Tax Authority. In practice, it may take several working days to a few weeks. Delays can happen if documents are incomplete or additional information is required. Your VAT obligations continue until approval is granted.

What if my business is being liquidated?

You are still required to complete VAT deregistration in UAE separately. VAT registration does not close automatically during liquidation. You must apply within the required timeframe after meeting the criteria to avoid administrative penalties.

Do I need a VAT deregistration letter?

A formal letter is not always required. However, the Federal Tax Authority may request a written explanation in certain cases. Preparing a simple VAT deregistration letter format UAE can help support your application if clarification is needed.

Closing: Staying Compliant Without Unnecessary Stress

Managing VAT deregistration in UAE comes down to timing, documentation, and following the correct process. When thresholds and deadlines are understood, the process becomes more straightforward and helps reduce the risk of administrative penalties under the rules set by the Federal Tax Authority.

A clear approach to preparing documents, completing filings, and submitting the application through the appropriate channels helps ensure that VAT obligations are properly closed. This reduces delays and supports a smoother transition out of VAT registration.

At MP Elites, we support UAE businesses with VAT compliance, including deregistration, filings, and coordination with the Federal Tax Authority. If you need clarity on the process or your next steps, professional guidance can help ensure everything is handled correctly.