Introduction

Most UAE businesses are familiar with the mandatory VAT registration threshold UAE of AED 375,000. However, businesses with taxable supplies, imports, or eligible taxable expenses exceeding AED 187,500 may qualify for voluntary VAT registration UAE, creating a strategic decision well before registration becomes compulsory.

For founders, finance managers, and growing SMEs, voluntary registration for VAT UAE is not simply a compliance question. Depending on the business model, customer base, and level of taxable expenses, early registration may support input VAT recovery, strengthen compliance readiness, and improve credibility with corporate clients. In other cases, the additional filing, record-keeping, and invoicing obligations may outweigh the benefits.

This guide explains the UAE VAT voluntary registration threshold, eligibility requirements, key advantages and drawbacks, and the business scenarios where registering early is likely to make strategic sense.

UAE VAT Registration: The Two Thresholds Explained

Understanding the VAT registration threshold UAE is the first step in assessing whether voluntary registration is worth considering.

The UAE VAT system operates with two registration thresholds:

| Registration Type | Threshold | Required? |

|---|---|---|

| Mandatory Registration | AED 375,000 | Yes |

| Voluntary Registration | AED 187,500 | No |

Under Federal Tax Authority (FTA) rules, businesses must register for VAT when taxable supplies and imports exceed AED 375,000 during the previous 12 months or are expected to exceed that amount within the next 30 days.

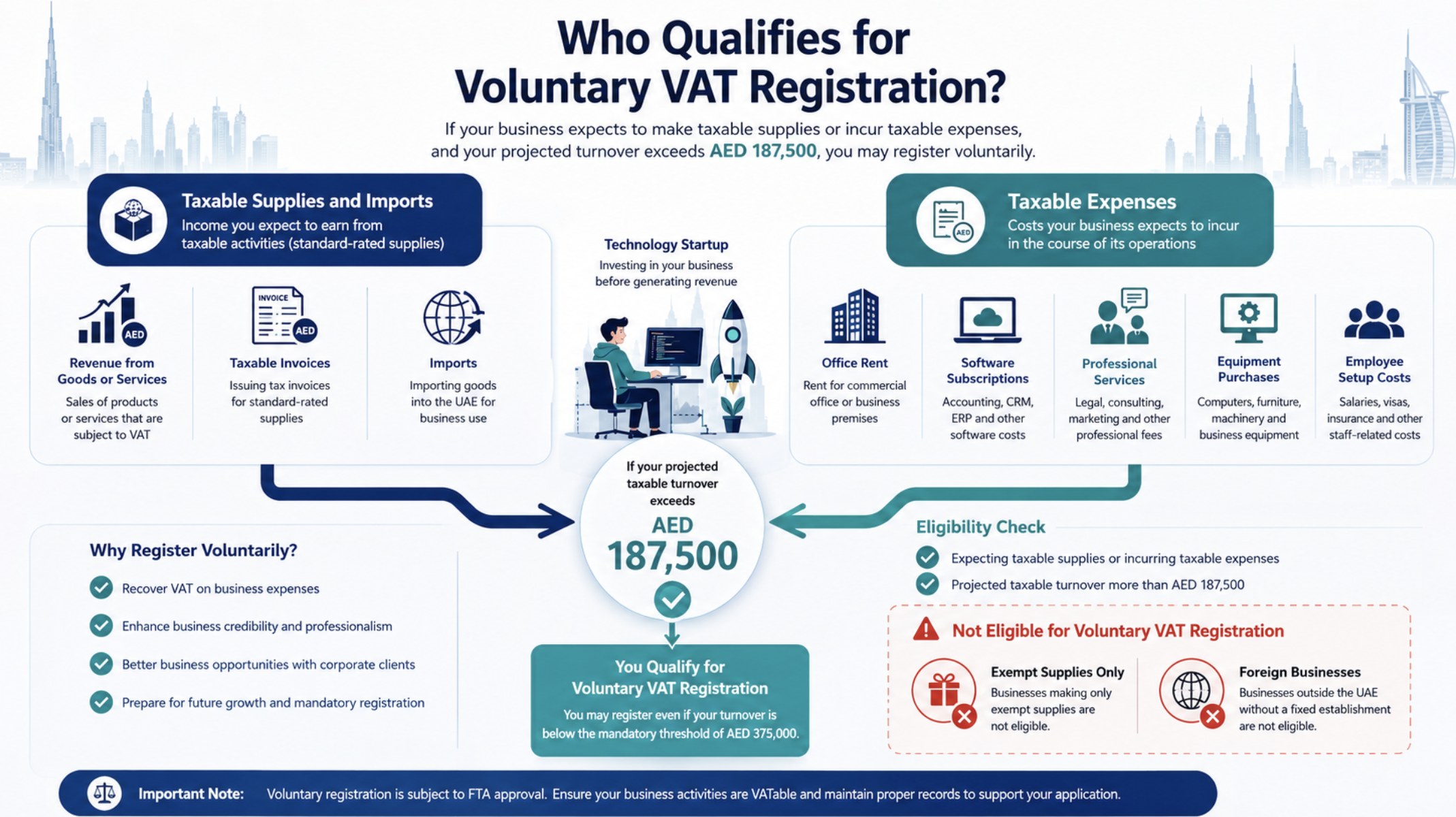

The voluntary VAT registration threshold UAE is AED 187,500. Businesses may apply for VAT registration when taxable supplies, imports, or qualifying taxable expenses exceed this amount. Registration at this level is optional rather than mandatory.

Exceeding the UAE VAT voluntary registration threshold does not create a legal obligation to register. Instead, it allows a business to evaluate whether VAT registration aligns with its commercial objectives, expense profile, and growth plans.

The next step is determining whether your business meets the eligibility requirements for voluntary VAT registration.

Who Is Eligible for Voluntary VAT Registration?

Understanding eligibility is the first step in deciding whether voluntary VAT registration UAE makes strategic sense for your business.

A UAE-based business may apply for voluntary registration for VAT UAE if any of the following apply:

- Taxable supplies exceed AED 187,500 during the previous 12 months.

- Taxable imports exceed AED 187,500 during the previous 12 months.

- Taxable supplies or imports are expected to exceed AED 187,500 within the next 30 days.

- Taxable business expenses exceed AED 187,500 during the previous 12 months or are expected to exceed that threshold within the next 30 days.

The expenses route is particularly relevant for pre-revenue startups and early-stage businesses that have incurred significant setup costs before generating substantial revenue. Examples may include:

- Office rent

- Equipment purchases

- Professional advisory fees

- Technology and operational setup costs

A business may qualify for UAE VAT voluntary registration through these expenses even if sales remain limited.

However, voluntary registration is not available to all businesses:

- Businesses making only exempt supplies are not eligible for VAT registration, whether mandatory or voluntary.

- Foreign businesses are generally not eligible to use the UAE’s voluntary registration regime.

For businesses asking what is voluntary registration for VAT, eligibility depends on taxable supplies, imports, or taxable expenses meeting the Federal Tax Authority’s AED 187,500 threshold.

The Strategic Case for Registering Early: Key Advantages

For eligible businesses, voluntary VAT registration UAE can be more than a compliance decision. Depending on the business model, registering before the mandatory threshold may provide commercial, operational, and cash-flow benefits.

Input VAT Recovery

One of the main advantages of voluntary VAT registration is the ability to recover input VAT paid on eligible business expenses before registration becomes mandatory.

Examples may include:

- Office rent

- Equipment and technology purchases

- Professional services

- Marketing and operational costs

For startups and growing SMEs investing heavily in expansion, recovering input VAT can reduce the overall cost of doing business.

B2B Credibility and Commercial Positioning

VAT registration can also strengthen credibility with corporate clients, government entities, and procurement-driven organisations. Many business customers expect suppliers to be VAT registered because they can recover input VAT on their purchases.

While VAT registration is not a requirement for winning contracts, a VAT-registered business is often viewed as a more established and compliance-focused organisation.

Growth Readiness Before the Mandatory Threshold

Businesses approaching the AED 375,000 mandatory threshold often need to implement VAT-compliant invoicing, accounting controls, record-keeping procedures, and reporting processes.

Choosing voluntary registration for VAT allows these systems to be established before registration becomes compulsory, reducing the risk of a rushed transition when the mandatory threshold is reached.

Benefits for Certain Free Zone Businesses

Some free zone businesses making qualifying zero-rated exports may be able to recover input VAT on eligible operating costs without charging output VAT on qualifying supplies.

For export-focused businesses, this can improve cost efficiency while maintaining compliance with UAE VAT requirements.

The strongest case for UAE VAT voluntary registration typically exists where a business has significant taxable expenses, serves B2B customers, or expects to exceed the mandatory AED 375,000 threshold in the near future.

When Voluntary Registration May Not Be the Right Move

Voluntary VAT registration UAE can offer strategic benefits, but it is not the right choice for every business. Eligibility alone does not mean registration will create meaningful commercial or financial value.

Situations where voluntary registration may be less advantageous include:

- B2C-heavy businesses: Charging 5% VAT on taxable sales increases the final price paid by consumers, who generally cannot recover VAT. For businesses operating below the mandatory AED 375,000 threshold, this may reduce price competitiveness against non-registered competitors.

- Businesses with limited compliance capacity: Once registered, a business must comply with all VAT obligations, including issuing FTA-compliant tax invoices, filing VAT returns on the schedule assigned by the Federal Tax Authority, and maintaining appropriate accounting records and supporting documentation.

- Early-stage businesses with low taxable expenses: Where recoverable input VAT is limited, the financial benefit of registration may not outweigh the ongoing administrative and compliance requirements.

When assessing voluntary VAT registration requirements, businesses should evaluate their customer base, taxable expenses, and growth plans rather than making the decision based solely on eligibility under the voluntary threshold.

SME and Startup Scenarios: A Decision Framework

The advantages of voluntary VAT registration depend on your business model, taxable expense levels, and growth plans rather than threshold proximity alone.

| Scenario | Typical Situation | Strategic Consideration |

|---|---|---|

| Scenario A — Pre-revenue startup with B2B clients | High setup costs, minimal revenue, significant spending on office rent, equipment, software, or professional services | Voluntary VAT registration UAE may allow input VAT recovery and support compliance credibility with early corporate clients. |

| Scenario B — Growing SME | Taxable supplies, imports, or expenses exceed AED 187,500 and business growth is accelerating | Early registration helps establish VAT-compliant invoicing and reporting processes before reaching the AED 375,000 mandatory threshold. |

| Scenario C — B2C-only retailer below AED 375,000 | Sales are primarily to consumers and recoverable input VAT is limited | Adding 5% VAT may affect price competitiveness, making voluntary registration less attractive unless taxable expenses are significant. |

| Scenario D — Free zone entity making zero-rated supplies | Export-focused business incurring VAT on procurement and operating costs | VAT voluntary registration UAE may support input VAT recovery without charging output VAT on qualifying zero-rated exports. |

The right decision depends on whether the benefits of registration outweigh the compliance obligations. Revenue model (B2B versus B2C), current expense levels, and future growth plans are typically more important considerations than the voluntary registration threshold alone.

Documentation Required for Voluntary VAT Registration

Businesses applying for voluntary registration for VAT UAE must provide documentation that confirms both their legal status and eligibility under the voluntary registration threshold.

Typical voluntary VAT registration requirements include:

- A current and valid trade licence

- Emirates ID and passport copies of the owner(s) or authorised signatory

- Proof that taxable supplies, imports, or taxable expenses exceed AED 187,500, such as invoices, contracts, purchase records, or bank statements

- Business bank account details

- Memorandum of Association (MOA) or equivalent incorporation documents

- Registered business address and contact details

For startups and businesses applying through the taxable-expenses route, supporting documentation should clearly demonstrate qualifying expenses incurred during the relevant period. Businesses should also ensure that broader compliance records, including Ultimate Beneficial Owner rules in the UAE, are properly maintained and up to date.

How to Complete Voluntary VAT Registration: Step-by-Step

Businesses applying for voluntary VAT registration UAE must submit their application through the Federal Tax Authority’s (FTA) EmaraTax platform. Preparing the required information and supporting documents in advance can help reduce processing delays.

Step 1: Create an EmaraTax Account

Access the EmaraTax portal and create an account using your business details. Businesses that already have an EmaraTax profile can log in using their existing credentials.

Step 2: Access the VAT Registration Application

After logging in, navigate to the VAT section and select the option to start a new VAT registration application. Ensure you choose the correct registration type before proceeding.

Step 3: Complete the Required Information

Enter the business information requested by the FTA, including legal structure, business activities, contact details, expected turnover, import or export activities, and bank account information. The details should match the company’s licensing and corporate records.

Step 4: Upload Supporting Documentation

Upload the documents required to support eligibility for voluntary registration for VAT UAE, including:

- Valid trade licence

- Emirates ID and passport copies of the owner or authorised signatory

- Proof of taxable supplies, imports, or taxable expenses exceeding AED 187,500

- Memorandum of Association (MOA) or equivalent formation documents

Step 5: Submit the Application

Review all information and supporting documents before submission. The FTA typically reviews VAT registration applications within 20 business days, although additional information may be requested in some cases.

Step 6: Receive Your TRN and Begin Compliance

Once approved, the business receives a Tax Registration Number (TRN). From that point, it must issue VAT-compliant tax invoices, maintain VAT records, and comply with ongoing filing obligations.

Businesses should also consider how VAT registration fits within their broader tax framework, including obligations covered in the UAE Corporate Tax return guide.

Obligations After Voluntary VAT Registration

Once approved for voluntary registration for VAT, a business assumes the same obligations as any other VAT-registered entity.

- Issue VAT-compliant tax invoices for all taxable supplies. Invoices must include the Tax Registration Number (TRN), VAT amount, and other information required by the Federal Tax Authority (FTA).

- File VAT returns on time. Most businesses are assigned quarterly filing periods, although some larger businesses may be required to file monthly returns.

- Maintain accounting records and supporting documents. VAT records, invoices, and related documentation must generally be retained for at least five years. Real estate-related records may need to be retained for up to 15 years. Proper recordkeeping also supports audit requirements in the UAE.

- Update FTA registration details when changes occur. Businesses should promptly update information such as their registered address, banking details, or nature of taxable activities.

- Follow the formal VAT deregistration process when eligible. A business may apply for deregistration if its taxable supplies and expenses fall below AED 187,500 and remain below that threshold for 12 consecutive months. Deregistration requires a formal application and FTA approval.

Frequently Asked Questions

Can a UAE startup with no revenue register for VAT voluntarily?

Yes. A startup may qualify if its taxable expenses exceed AED 187,500 in the previous 12 months or are expected to exceed that amount within the next 30 days. This commonly applies to businesses incurring significant setup costs such as office rent, equipment, or professional services.

What is the voluntary VAT registration threshold in the UAE?

The voluntary VAT registration threshold in the UAE is AED 187,500. Businesses that meet this level through taxable supplies, imports, or taxable expenses may apply for VAT registration. Mandatory registration applies at AED 375,000.

What are the main advantages of voluntary VAT registration for a UAE SME?

Key advantages include recovering input VAT on eligible business expenses, improving credibility with B2B customers, and establishing VAT-compliant processes before mandatory registration becomes necessary.

How long does FTA approval for voluntary VAT registration take?

The Federal Tax Authority (FTA) typically reviews applications within 20 business days, provided the application and supporting documents are complete.

Can a voluntarily registered UAE business deregister from VAT later?

Yes. A business may apply for VAT deregistration if its taxable supplies and expenses remain below AED 187,500 for 12 consecutive months. Deregistration requires FTA approval.

Does voluntary VAT registration apply to businesses in UAE free zones?

Yes. Eligible free zone businesses can apply for VAT registration if they meet the relevant threshold requirements. This may be beneficial for businesses making qualifying zero-rated exports that wish to recover input VAT on expenses.

Is Voluntary VAT Registration the Right Strategic Move?

Voluntary VAT registration UAE is a strategic decision, not simply a threshold calculation. The right approach depends on your revenue model, taxable expenses, growth plans, and compliance requirements.

For some businesses, early registration supports input VAT recovery, stronger B2B credibility, and smoother preparation for future growth. For others, the additional compliance obligations may outweigh the immediate benefits.

If you need support with VAT registration, compliance, or ongoing filing obligations, explore our VAT services.

Ready to evaluate the best approach for your business? Request a strategic assessment and speak with the MP Elites team about your VAT, Corporate Tax, and compliance requirements.