Introduction

Missed VAT return reconciliations, uncategorised transactions piling up before a Corporate Tax filing deadline, and years of backlogged entries can leave financial records unreliable. The good news is that a bookkeeping cleanup can fix these issues. If you are wondering how to clean up messy bookkeeping, the process starts with identifying errors, reconciling accounts, and restoring accurate accounting & bookkeeping in UAE operations.

UAE businesses face strict compliance obligations under the Federal Tax Authority (FTA) and the Ministry of Finance (MoF) Corporate Tax regime. Inaccurate records can delay tax preparation, undermine financial reporting, and make it difficult to support business decisions with confidence.

This guide provides a practical, step-by-step bookkeeping cleanup process to help UAE businesses organise records, correct bookkeeping errors, reconcile accounts, and prepare for VAT and Corporate Tax compliance.

Why UAE Businesses End Up with Messy Books

Messy financial records rarely result from a single mistake. In most cases, bookkeeping issues develop gradually as business activity increases and record-keeping processes fail to keep pace.

Common causes include:

- Rapid growth that increases transaction volumes faster than existing bookkeeping processes can handle.

- Switching accounting software mid-year, which can create duplicate accounts, missing transactions, or incomplete historical records if data is not migrated correctly.

- Mixing personal and business transactions, making it difficult to track business performance and maintain accurate financial records.

- Incomplete VAT transaction records, including missing tax invoices, unreconciled VAT accounts, and transactions that have not been properly categorised.

Many UAE businesses also began operating before the introduction of Corporate Tax and never established a compliant record-keeping structure designed for VAT and tax reporting requirements. As Corporate Tax filing obligations have become part of the compliance landscape, these historical weaknesses are becoming more visible.

This highlights the importance of bookkeeping for UAE businesses. For bookkeeping for SMEs in UAE, limited resources and delayed record-keeping often allow small issues to accumulate until a VAT return, audit request, financing application, or Corporate Tax filing deadline forces a full cleanup.

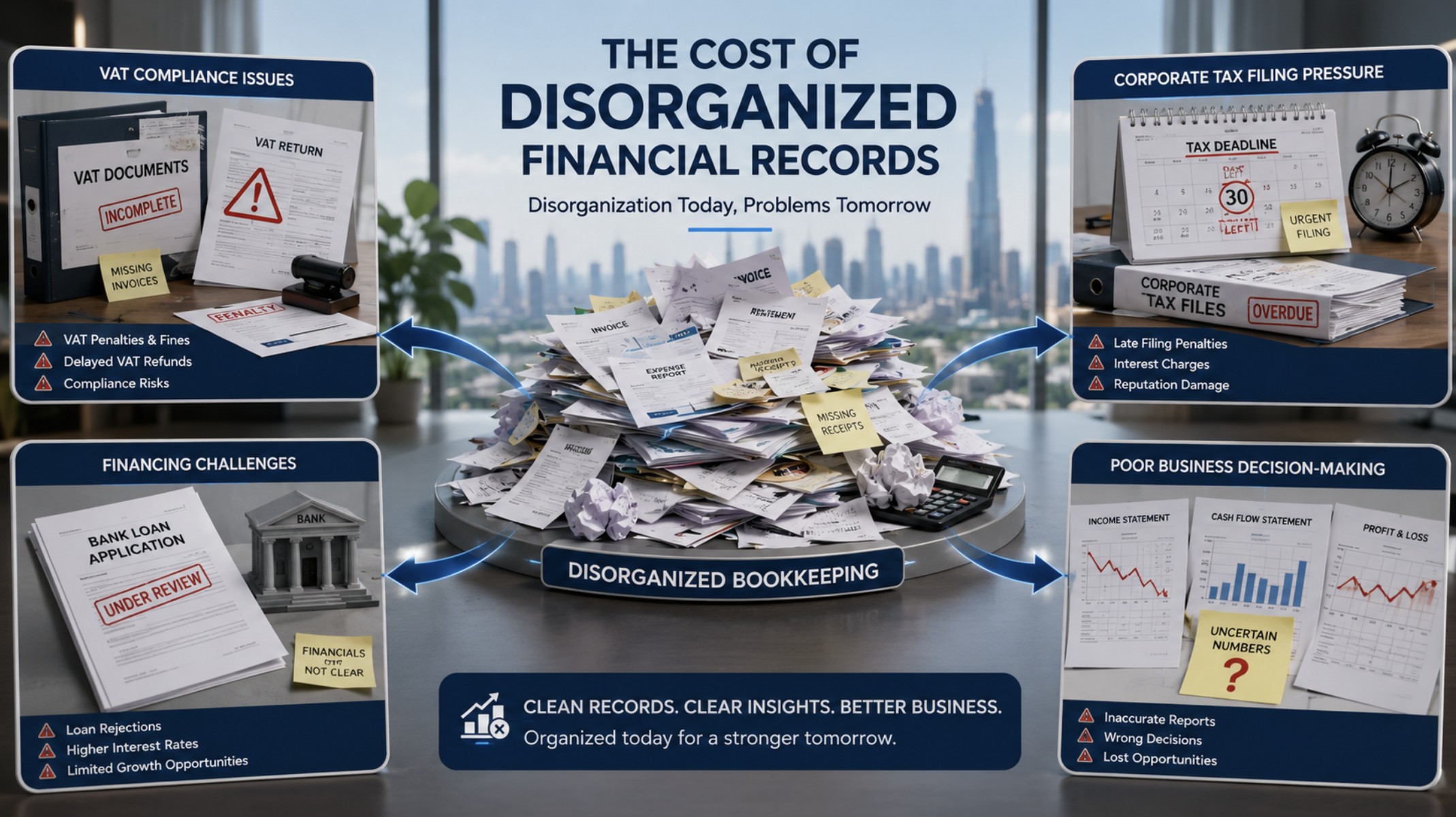

The Real Cost of Disorganised Records in the UAE

Disorganised financial records create more than administrative headaches. They increase compliance risk, delay tax filings, and can affect a business’s ability to secure financing or satisfy due diligence requests.

Disorganised financial records create more than administrative headaches. They increase compliance risk, delay tax filings, and can affect a business’s ability to secure financing or satisfy due diligence requests.

Common consequences include:

- FTA VAT audit exposure when tax invoices, VAT reconciliations, or supporting transaction records are incomplete.

- Corporate Tax filing errors caused by inaccurate financial statements, unreconciled accounts, or incorrect taxable income calculations.

- Late filing or payment penalties when bookkeeping issues delay VAT or Corporate Tax preparation.

- Blocked or delayed bank financing where lenders cannot verify the business’s financial position.

- Difficulty securing trade finance due to incomplete or unreliable financial records.

- Investor due diligence concerns when historical accounts cannot be supported by underlying documentation.

These risks highlight the importance of bookkeeping for UAE businesses. Effective accounting & bookkeeping in UAE organisations supports VAT compliance, Corporate Tax reporting, financing applications, audit readiness, and stronger financial controls. Maintaining organised records also helps businesses meet UAE audit requirements for businesses and respond more efficiently to financial reviews and compliance checks.

The urgency is amplified by fixed compliance deadlines. VAT return cycles and the UAE Corporate Tax filing window leave limited time to resolve historical bookkeeping issues once reporting preparations begin. The longer records remain disorganised, the more difficult and resource-intensive the cleanup process becomes.

Step 1: Assess the Scope of the Cleanup

Before making corrections, determine the full scope of the bookkeeping cleanup. This helps establish priorities, estimate the workload, and identify gaps that may affect VAT or Corporate Tax reporting.

Start by defining the cleanup period. Some businesses may only need to correct a few months of missing entries, while others may be dealing with one or more years of backlogged records.

Review the accounting system and identify:

- Missing accounts that should exist but are not reflected in the records

- Duplicate accounts created during software migrations or historical bookkeeping changes

- Unreconciled bank, credit card, loan, or balance sheet accounts

VAT records should also be assessed at this stage. Confirm that:

- VAT input and output transactions have been recorded correctly

- Supporting tax invoices are available

- Reported VAT figures can be traced to underlying transactions

Finally, determine whether the project involves a one-period catch-up or a multi-year backfill requiring reconstruction of historical records and supporting documentation.

Outcome: A defined cleanup period, a list of missing or unreconciled accounts, and a clear understanding of the work required to complete the bookkeeping cleanup.

Step 2: Organise and Gather Source Documents

Once the cleanup scope has been defined, gather the documents needed to support reconciliations, corrections, and tax reporting. Missing or incomplete records can slow down the cleanup process and make it difficult to verify historical transactions.

Collect and organise:

- Bank statements for all business accounts

- Credit card statements

- Customer and supplier invoices

- VAT-registered supplier receipts

- Payroll records, including WPS documentation where applicable

- FTA-compliant tax invoices

- Customs duty receipts and supporting documents for import transactions

As documents are collected, store them in a structured digital filing system. Files should be named and organised to match transaction dates and reporting periods, making them easier to trace during reconciliations, VAT reviews, and future audits.

To support FTA record-retention requirements, businesses should retain relevant tax and accounting records for a minimum of five years.

Before moving to the reconciliation stage, identify any missing statements, invoices, tax invoices, or payroll records and obtain replacement copies where available.

Outcome: Source documents are organised, accessible, and matched to the relevant transaction periods, creating a reliable foundation for the bookkeeping cleanup process.

Step 3: Reconcile Every Account

Reconciliation verifies that the accounting records match the underlying financial activity. This step often uncovers errors that affect financial reporting, VAT compliance, and Corporate Tax preparation.

Review each account and match transactions against the relevant bank or credit card statement. Every payment, receipt, transfer, and fee should be supported by a corresponding entry in the accounting records.

During the reconciliation process, identify and resolve:

- Duplicate entries

- Missing transactions

- Misposted credits or payments

- Incorrect posting dates

- Uncleared cheques that remain outstanding without explanation

VAT accounts should be reconciled separately. Compare VAT liability balances against previously filed VAT returns to confirm that reported amounts agree with the underlying transactions and supporting documentation.

Flag any reporting periods where VAT returns were submitted but the supporting invoices or transaction records cannot be located. These gaps should be investigated and documented before future VAT reviews, audits, or tax filings.

Outcome: Account balances are reconciled, discrepancies are resolved, and financial records are supported by verifiable documentation.

Step 4: Fix the Chart of Accounts

After reconciling accounts, review the chart of accounts to ensure it supports accurate financial reporting, VAT compliance, and Corporate Tax calculations. A poorly structured chart of accounts can create reporting errors even when transactions have been recorded correctly.

As part of the cleanup bookkeeping process:

- Merge duplicate accounts created through software migrations or inconsistent bookkeeping practices.

- Remove unused or obsolete categories that no longer reflect current business activities.

- Rename accounts for clarity and consistency so transactions are categorised correctly going forward.

For bookkeeping cleanup UAE projects, the chart of accounts should also support UAE tax reporting requirements. VAT-related accounts should clearly separate input VAT, output VAT, and VAT payable balances to simplify reconciliations and support accurate VAT return preparation.

Expense categories should be reviewed to ensure costs are classified appropriately for UAE Corporate Tax purposes. The account structure should allow businesses to distinguish between deductible and non-deductible expenses when calculating taxable income and preparing supporting tax records.

The goal is a clean, standardised chart of accounts that produces reliable financial information and supports ongoing compliance requirements.

Outcome: A structured chart of accounts aligned with VAT reporting, Corporate Tax calculations, and day-to-day bookkeeping requirements.

Step 5: Review Accounts Payable, Receivable, and Payroll

Review accounts receivable and accounts payable balances to ensure outstanding invoices are accurately recorded and properly aged. Long-outstanding customer balances should be assessed for recoverability. Where a receivable is genuinely uncollectable, businesses should consider appropriate write-off treatment before the relevant Corporate Tax period closes.

Payroll records should be reconciled against UAE Wage Protection System (WPS) reports to confirm that salary expenses recorded in the accounting system match actual payroll payments.

Employee-related liabilities should also be reviewed. Reconcile end-of-service benefit accruals against HR records to ensure obligations are accurately reflected in the financial statements.

For bookkeeping for SMEs in UAE, these reviews help ensure financial records are complete, accurate, and ready for reporting requirements. Accurate accounting & bookkeeping in UAE businesses depends on payroll, receivable, payable, and employee-liability balances being fully supported and up to date.

Outcome: Accounts receivable, accounts payable, payroll records, and employee-related liabilities accurately reflect the business’s current financial position.

Preparing Clean Books for UAE Corporate Tax and VAT Filing

A completed bookkeeping cleanup should result in financial records that are ready to support VAT compliance, Corporate Tax reporting, and year-end financial statement preparation.

Before filing begins, businesses should review key accounting records, including:

- The trial balance to identify unusual balances or unresolved discrepancies.

- Adjusted journal entries for accruals, depreciation, and corrections identified during the cleanup process.

- Retained earnings balances to ensure prior-year results have been carried forward accurately.

For businesses looking to prepare books for tax filing UAE requirements, these reviews help ensure financial statements and tax calculations are based on reliable data.

From a VAT perspective, reconciled records improve VAT return accuracy by ensuring VAT liability balances agree with underlying transactions and supporting documentation. Missing invoices, unreconciled VAT accounts, or incorrect transaction classifications can create issues during return preparation and future reviews.

The same principle applies to UAE Corporate Tax return filing. Following the end of a financial year, UAE Corporate Tax returns are generally due within nine months. Businesses that postpone bookkeeping cleanup until the filing window is approaching often discover:

- Unreconciled accounts.

- Missing supporting documents.

- Historical posting and categorisation errors.

- Inaccurate retained earnings balances.

These issues can delay return preparation, increase correction work, and create additional compliance risks.

This is why bookkeeping cleanup UAE projects should be completed well before VAT return deadlines and Corporate Tax filing periods. Clean books make it easier to calculate taxable income, support reported figures, and prepare accurate financial information for compliance, audit, financing, or due diligence purposes.

Bookkeeping Cleanup Checklist for UAE Businesses

Use this bookkeeping cleanup checklist to confirm that key records and compliance requirements have been addressed:

- Define the cleanup period and identify how far behind the books are.

- Gather bank statements, invoices, payroll records, VAT documentation, and supporting records.

- Reconcile all bank and credit card accounts.

- Verify VAT liability balances against filed VAT returns.

- Resolve duplicate, missing, or incorrectly categorised transactions.

- Review and update the chart of accounts.

- Review accounts receivable, accounts payable, payroll records, and end-of-service accruals.

- Reconcile payroll entries against UAE Wage Protection System (WPS) records.

- Review the trial balance and post any required adjustments.

- Confirm the books are ready to support VAT and Corporate Tax reporting.

When to Call a Professional

Consider professional support if:

- The books are more than 12 months behind.

- An FTA audit notice has been received.

- A UAE Corporate Tax return is due within the next 60 days.

- Multiple reporting periods contain missing source documents.

- Significant VAT discrepancies have been identified.

Businesses that need support with historical reconciliations, VAT reviews, or ongoing bookkeeping maintenance may benefit from MP Elites bookkeeping services.

If your business is dealing with historical bookkeeping issues, VAT reconciliations, or upcoming Corporate Tax deadlines, contact MP Elites to discuss the next steps and build a reliable foundation for future compliance and reporting.

Disclaimer: This article is provided for general informational purposes only and should not be considered accounting, tax, or legal advice. Businesses should consult a qualified UAE accountant or tax professional regarding their specific circumstances.

Frequently Asked Questions

What does a bookkeeping cleanup involve for a UAE business?

A bookkeeping cleanup involves reviewing and correcting historical financial records to ensure they support accurate VAT reporting, Corporate Tax calculations, and financial reporting. This typically includes reconciling bank accounts, resolving categorisation errors, reviewing VAT records, correcting duplicate or missing transactions, and updating the chart of accounts.

How long does a bookkeeping cleanup take?

The timeframe depends on the volume and condition of the records. A business that is only a few months behind may require a straightforward catch-up exercise, while records that are 6–12 months behind often require a more detailed review. Multi-year backlogs generally require a full reconstruction of historical transactions and supporting documents.

Do I need to clean up my books before filing a UAE Corporate Tax return?

In most cases, yes. Corporate Tax calculations rely on accurate financial records. Completing a bookkeeping cleanup before preparing a tax return helps identify unreconciled accounts, incorrect expense classifications, and other issues that may affect reporting accuracy. UAE Corporate Tax returns are generally due within nine months of the end of the relevant financial year.

What records does the FTA require businesses to retain for VAT purposes?

Businesses should retain records supporting VAT transactions, including tax invoices, credit notes, supplier invoices, bank statements, accounting records, and customs documentation where applicable. VAT-related records should generally be retained for at least five years in accordance with UAE record-retention requirements.

Can messy bookkeeping trigger a UAE VAT audit?

Messy bookkeeping does not automatically trigger an audit. However, missing supporting documents, unreconciled VAT balances, and inconsistencies between VAT returns and accounting records can increase compliance risk and make it more difficult to support reported figures during an FTA review.

What is the difference between bookkeeping cleanup and standard monthly bookkeeping?

Bookkeeping cleanup focuses on correcting historical issues such as unreconciled accounts, VAT discrepancies, duplicate transactions, and reporting errors. Standard monthly bookkeeping is an ongoing process that records, categorises, and reviews transactions regularly to maintain accurate financial records going forward.