Last reviewed: April 2026

Small business relief UAE is a provision under the UAE corporate tax regime that allows eligible businesses to be treated as having no taxable income, provided specific conditions are met. It is designed to reduce the tax and compliance burden for small and medium-sized businesses while keeping them within the corporate tax system.

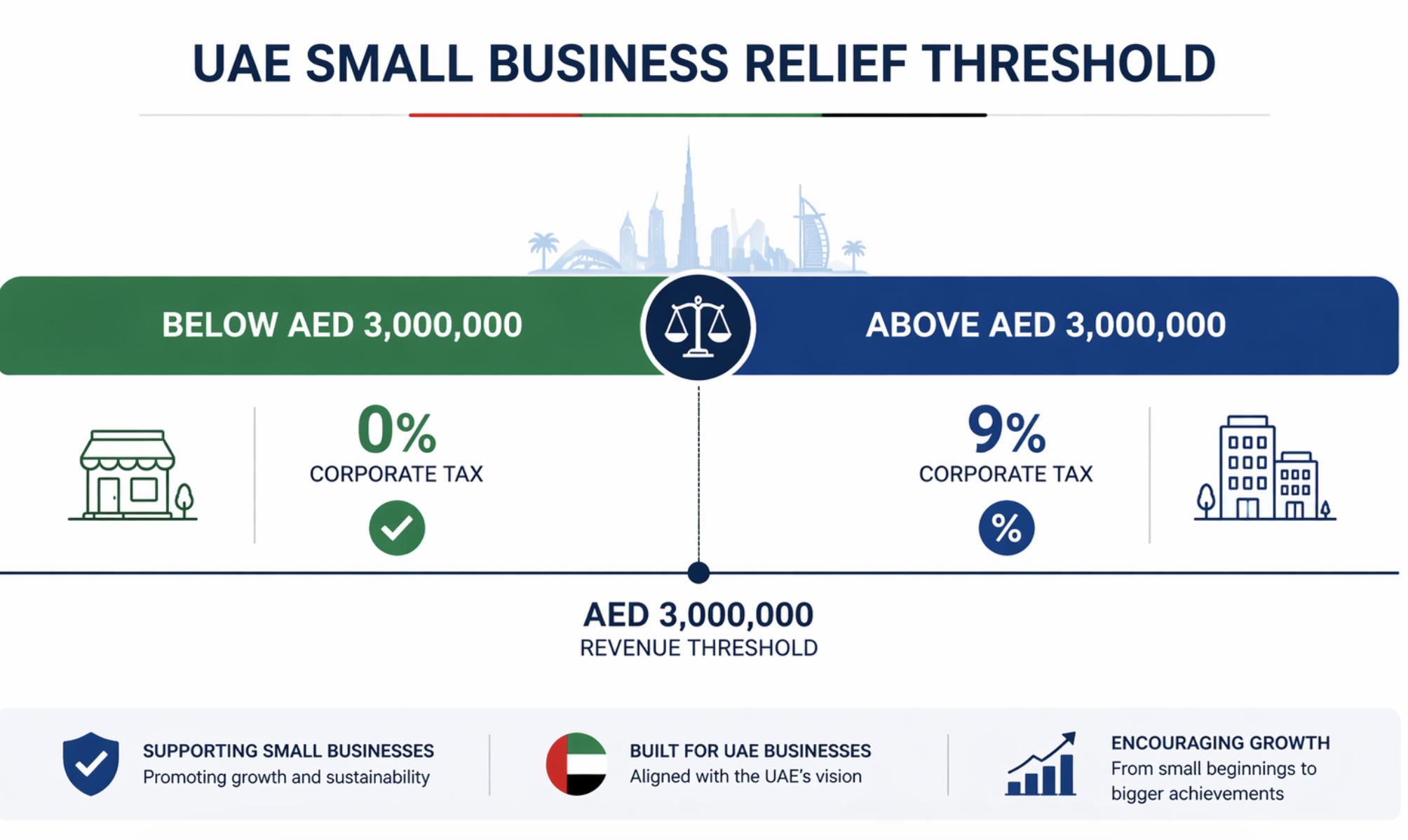

This relief matters because the standard UAE corporate tax rate is 9% on taxable income above the applicable threshold. Businesses that qualify for UAE small business relief may apply a 0% outcome for corporate tax purposes. However, eligibility is not automatic. Businesses must assess their revenue, meet the defined criteria, and make a valid election in their tax return.

This guide is for UAE business owners, SME finance managers, and independent professionals who want a clear and practical understanding of small business relief in UAE corporate tax, including eligibility, the AED 3,000,000 revenue threshold, and how to apply correctly.

What Is UAE Small Business Relief?

UAE small business relief is a provision under Federal Decree-Law No. 47 of 2022 on Corporate Tax. It allows eligible businesses to be treated as having no taxable income for a specific tax period, provided they meet the required conditions.

Under this relief, a qualifying business does not pay corporate tax for the relevant period. However, the business must still register for corporate tax and submit its tax return. The relief does not remove compliance obligations.

To qualify, a business must have revenue of AED 3,000,000 or less for the relevant tax period. This threshold applies to each tax period and is available for periods ending on or before 31 December 2026, based on current Federal Tax Authority guidance.

Small business relief UAE corporate tax is not applied automatically. A business must elect to apply the relief when filing its corporate tax return. Failure to make this election means the business will be subject to standard corporate tax rules.

Who Is Eligible for Small Business Relief in UAE?

Eligibility for UAE small business relief depends on the legal status of the business, its tax residency, and whether it meets specific conditions set under the UAE corporate tax framework.

Eligible Businesses

A business may qualify for UAE corporate tax small business relief if it falls into one of the following categories:

- A resident juridical person, such as a UAE-incorporated company

- A natural person conducting a business or commercial activity in the UAE, including freelancers and sole proprietors

Key Eligibility Criteria

To claim small business relief UAE corporate tax, the business must meet all of the following conditions:

- It must be a UAE tax resident for corporate tax purposes

- It must have revenue of AED 3,000,000 or less in the relevant tax period

- It must make a valid election in its corporate tax return

Excluded Businesses

A business will not qualify for small business relief in UAE corporate tax if it falls into any of the following categories:

- A Qualifying Free Zone Person

- A member of a multinational enterprise group subject to global minimum tax rules

- A member of a qualifying group under UAE corporate tax provisions

Businesses should assess their classification and structure carefully before applying the relief. Incorrect assumptions about eligibility may lead to non-compliance or incorrect tax filings.

Revenue Threshold and the Election Process

Understanding the revenue threshold and election process is essential when applying small business relief UAE corporate tax rules. Both determine whether a business qualifies and whether the relief is applied correctly.

What Counts Toward the AED 3 Million Threshold?

The AED 3,000,000 threshold is based on total revenue, not net profit. A business must assess its gross income for each tax period to determine eligibility.

Revenue generally includes:

- Income from core business activities

- Revenue from goods sold or services provided

- Other business-related income

A business that exceeds AED 3,000,000 in revenue during a tax period will not qualify for UAE small business relief for that period. Profit levels do not affect this threshold.

Annual Election Requirement

Applying UAE corporate tax small business relief requires a formal election. This election must be made for each tax period.

- The business must elect the relief when filing its corporate tax return

- The election is submitted through the EmaraTax system

- The election does not carry forward automatically

If a business meets the eligibility criteria but does not make the election, the relief will not apply. The business will be subject to standard corporate tax rules.

Timing and Consequences

The election must be made within the corporate tax filing deadline set by the Federal Tax Authority.

If the deadline is missed:

- The business cannot apply small business relief in UAE corporate tax for that period

- The business will be taxed under the standard 9% corporate tax rate

If revenue exceeds AED 3,000,000 in any tax period, the business will not qualify for that period. Future eligibility depends on whether revenue falls within the threshold in subsequent periods.

Related Parties and Aggregation

Businesses that operate through multiple entities or have related parties must review their structure carefully.

Artificial arrangements designed to split revenue across entities to remain below the AED 3,000,000 threshold may not be accepted under UAE corporate tax rules. The Federal Tax Authority expects business structures to reflect genuine commercial activity.

UAE small business relief reduces the corporate tax burden for eligible businesses. However, it does not remove core compliance responsibilities. You should understand both what the relief provides and what obligations still apply.

What You Are Relieved From

If you qualify for small business relief UAE corporate tax and make a valid election, your business is treated as having no taxable income for that tax period.

This means:

- You should not pay corporate tax for that period

- You are not required to calculate taxable income for corporate tax purposes

The relief applies only if you meet all eligibility conditions and elect it in your corporate tax return.

What You Must Still Do

Even if you apply UAE corporate tax small business relief, you should continue to meet all compliance requirements.

You should:

- Register for corporate tax with the Federal Tax Authority

- Maintain accurate accounting records and supporting documents

- File a corporate tax return for each tax period

- Ensure all financial information is complete and accurate

The relief does not remove filing or record-keeping obligations. The Federal Tax Authority may review your submission to confirm eligibility.

Key Consideration

You should treat small business relief in UAE corporate tax as a compliance mechanism, not an exemption from the system. Failure to meet registration, filing, or record-keeping requirements may result in penalties, even if no tax is payable.

Practical SME Scenarios

The following examples show how UAE small business relief applies in common business situations. Each scenario highlights eligibility, compliance requirements, and practical considerations.

Scenario 1: Consultancy Firm (AED 2.1 Million Revenue)

A Dubai-based consultancy generates AED 2.1 million in annual revenue.

- Revenue is below the AED 3,000,000 threshold

- The business qualifies for small business relief UAE corporate tax

- The business must still register and file a corporate tax return

Practical approach: The business should elect the relief in its tax return. This removes the corporate tax liability for the period while maintaining full compliance.

Scenario 2: Freelancer (AED 800,000 Income)

A freelance designer earns AED 800,000 from business activities during the year.

- The individual is treated as a natural person conducting business

- Revenue is within the eligibility threshold

- Corporate tax registration and filing are still required

Practical approach: The individual should apply UAE corporate tax small business relief through the tax return. This allows a 0% tax outcome while meeting all filing obligations.

Scenario 3: Trading Company (AED 2.9 Million Revenue)

A trading company reports AED 2.9 million in revenue for the tax period.

- Revenue is within the AED 3,000,000 threshold

- The business qualifies for relief for the current period

- The business is close to exceeding the threshold

Practical approach: The business should elect the relief for the current period and monitor revenue closely. If revenue exceeds AED 3,000,000 in a future period, the business will no longer qualify and will be subject to standard corporate tax rules.

These scenarios show that small business relief in UAE corporate tax depends on both eligibility and timing. Businesses must assess their revenue each period and plan ahead to maintain compliance.

How to Claim Small Business Relief in UAE?

Understanding how to apply for small business relief UAE requires following a clear process. The relief is not automatic. A business must complete each step correctly to ensure it applies.

Step 1: Register for Corporate Tax

A business must register for corporate tax through the EmaraTax portal.

- Registration is required even if no tax is expected to be payable

- The business must obtain a corporate tax registration number

Failure to register may result in penalties, regardless of eligibility for relief.

Step 2: Prepare Financial Records

Before filing, the business must confirm that it meets the eligibility requirements.

- Verify that total revenue does not exceed AED 3,000,000 for the relevant tax period

- Ensure financial records are accurate and complete

- Review eligibility criteria under UAE corporate tax rules

Accurate records are required to support the election and any future review by the Federal Tax Authority.

Step 3: Elect the Relief in the Tax Return

To apply UAE corporate tax small business relief, the business must make an election in its corporate tax return.

- The election is made during the filing process through EmaraTax

- No separate application form is required

- The relief must be selected for each tax period

If the election is not made, the business will be taxed under standard corporate tax rules.

Step 4: Submit the Return and Maintain Compliance

After making the election, the business must complete its filing and maintain proper documentation.

- Submit the corporate tax return within the required deadline

- Retain supporting documents, including invoices and financial statements

- Ensure all reported information is accurate and consistent

The Federal Tax Authority may review submissions to confirm eligibility. Businesses must be able to support their reported figures.

FREQUENTLY ASKED QUESTIONS

What happens if I exceed AED 3 million in revenue during the year?

The AED 3,000,000 threshold is assessed based on total revenue for the tax period. If you exceed this amount, you will not qualify for small business relief UAE for that period and will be subject to standard corporate tax rules. Eligibility is assessed separately for each period, so you may qualify again if you meet the conditions.

Can I elect small business relief every year?

Yes. You may apply UAE corporate tax small business relief for each tax period if you meet the eligibility criteria. The election must be made in your corporate tax return each year and does not carry forward automatically. If you do not make the election, the relief will not apply.

Is small business relief automatic in the UAE?

No. Small business relief UAE is not automatic. You must elect the relief when filing your corporate tax return through the EmaraTax system. If you do not select it, your business will be subject to standard corporate tax rules.

Does small business relief apply to free zone companies?

In general, a Qualifying Free Zone Person is not eligible to claim small business relief in UAE corporate tax. Free zone entities follow specific tax rules, so you should assess your classification carefully.

What records must I keep to support my claim?

You should maintain accurate financial records for each tax period, including revenue records, invoices, and financial statements. Even if you qualify for UAE small business relief, you must file a tax return and be able to support your figures if reviewed by the Federal Tax Authority.

Final Thoughts

Small business relief UAE requires careful assessment, timely election, and ongoing compliance. Meeting the AED 3,000,000 threshold alone is not sufficient. You must ensure all conditions are met and the relief is applied correctly.

Maintaining clear records and reviewing your position each tax period helps reduce risk and supports compliance. As revenue changes, you should plan ahead.

MP Elites supports UAE-based SMEs, freelancers, and growing businesses with clear and practical corporate tax guidance. If you need support with eligibility or applying the relief, professional advice can help ensure accuracy.